Executive Summary

The concept of qualified borrowers ("QBs") is widespread in the subscription line credit facility ("Subscription Facility") market. With an established and robust guarantee structure, the risk profile of including a QB option in a Subscription Facility is negligible for lenders (but comes with some administrative burden). In surveying Subscription Facilities over the last two years, the majority includes a QB concept.

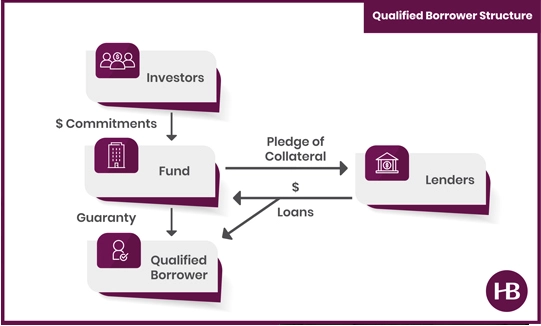

I. What is a Qualified Borrower?

In Subscription Facilities, QBs are generally portfolio companies, holding companies, special purpose vehicles, investment vehicles or other affiliate subsidiaries directly or indirectly controlled/owned by an entity that is a borrower or a guarantor in such Subscription Facility (the "Fund"). One key to a QB structure’s success is that the Fund must be permitted, via its governing documents, to guarantee the obligations of the QBs since QBs do not provide any security or credit support and are typically only severally liable. Instead, the Fund fully and unconditionally guarantees the obligations of QBs under a Subscription Facility and is liable for all loans made to such QBs.

II. How prevalent are Qualified Borrower structures in Subscription Facilities?

Approximately 71 percent of the Subscription Facilities we worked on over the last two years have a QB concept built into the loan documents. Lenders tend to offer (or Funds may request) this option in order to provide maximum flexibility and opportunity to fully utilize the Subscription Facility. However, only about 28 percent of Subscription Facilities with a QB structure had utilized such structure within two years of closing.

III. What is the purpose of joining a Qualified Borrower?

Joining a Subscription Facility provides QBs a direct source of liquidity in an economical and efficient manner. This can eliminate the need for a Fund to use its own capital to make an equity investment in, or an interfund loan to, a QB, thereby reducing administrative and organizational burdens for the Fund.

Additionally, when Funds want to incur debt at the QB level but may be unable to on a standalone basis, the optionality of adding the QB to its Subscription Facility provides quick liquidity solutions that would otherwise be unavailable. There may also be tax advantages related to direct borrowings by the QB (in lieu of interfund loans or equity investments) and the QB may be able to borrow at a lower rate under the Subscription Facility than it could through its own debt facility. Further, adding additional borrowers (whether QBs or otherwise) can create greater opportunity to increase utilization of the Subscription Facility.

IV. Conclusion.

In making loans to QBs, lenders find themselves supported by the same collateral pledged under the Subscription Facility as supports loans to the Fund, since the loans are fully and unconditionally guaranteed by the Fund and secured by the Fund’s collateral, in addition to being recourse to the underlying QB. Given the potential for significant liquidity benefits to the Fund and its QBs, coupled with the potential for greater utilization of the Subscription Facility without increasing risk profile for lenders, QB structures can be a helpful feature for Funds, QBs and lenders.

These insights are based on data from Subscription Facilities documented by Haynes Boone during the referenced period.

For more information on fund finance market trends, please reach out to any member of the Haynes Boone Fund Finance Practice Group.

For additional news and insights, please subscribe to our email list.