Introduction

Concentration limits are a familiar risk-management tool for lenders in subscription line facilities. By capping the amount of borrowing base credit that can be attributed to any single investor or group of related investors, lenders can protect themselves from outsized exposure to a small pool of investors and therefore diversify risk. But borrowers may require some flexibility in the application of such concentration limits to meet their borrowing needs, particularly if the borrower is still in its initial fundraising stages.

As a compromise to balance these priorities, lenders may agree to delay the application of concentration limits in a borrowing base in a subscription line credit facility (a “Concentration Limit Holiday”) to give the borrower an opportunity to further diversify its investor pool through additional investor closings.

While not uniformly adopted, borrowers and lenders have developed certain market standards regarding the documentation of delayed application of concentration limits in subscription line credit facilities. Given the current difficult and prolonged fundraising environment, and with many funds seeking subscription line facilities during the fundraising period, these Concentration Limit Holidays are becoming slightly more common.

Facts and Figures

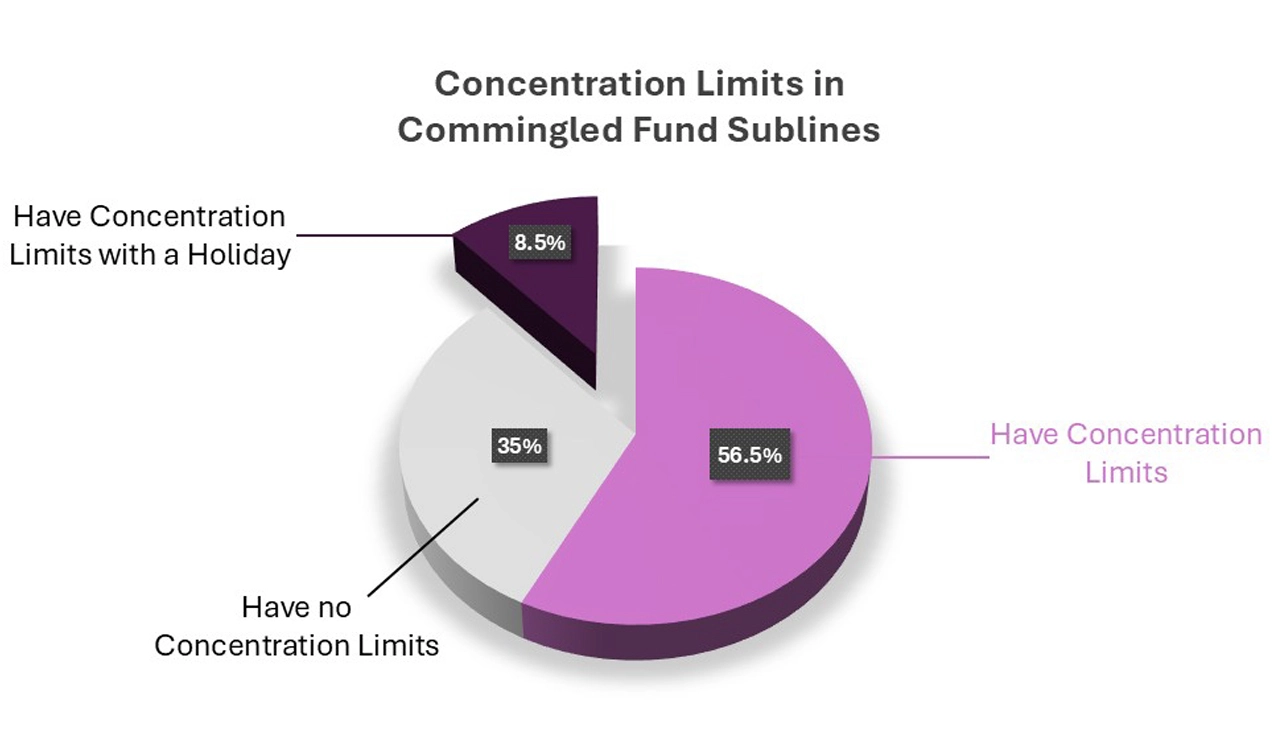

- Approximately 56.5 percent of the subscription line facilities we work on for commingled funds include some form of concentration limits, with another 8.5 percent containing a concentration limit with some form of Concentration Limit Holiday.

- Within the subset with Concentration Limit Holidays, there were holidays that absolutely waived the concentration limits until after the final close or some other date, while others applied more borrower-friendly concentration limits until a stated future date.

Concentration Limit Considerations

Concentration limits may apply to target categories of investors or specific investors in the collateral pool. Parties most often consider the following factors when negotiating concentration limits and related holiday periods:

- Timing of fundraising: What is the period during which the fund anticipates holding closings with investors, until a final closing at which point the characteristics of the pool of investors will be essentially fixed?

- Fundraising projections: The aggregate commitment size will influence whether parties find a concentration limit is necessary.

- Size, diversity and other characteristics of the investor base and individual investors, initially and as anticipated after the final closing. These are key determinants as to whether concentration limits are needed and how they should be targeted for the individual fund.

- Composition of the investor pool as to creditworthiness. A typical concentration limit scheme will provide generous limits for the most creditworthy investors, with small percentages for investors for which little financial information is available, or high-net-worth investors. Before the final closing, the pool is likely to be lopsided in one way or another depending on what investors happen to close in the earlier stages.

- Specific investor concerns: If a specific investor has problematic language in their investor documentation or a unique risk profile, lenders may want to apply a specific concentration limit to that investor to limit exposure.

Once concentration limits are established, consent of all lenders in the facility is usually required to relax or waive the concentration limits. However, the administrative agent may have discretion to assign a concentration limit within a pre-defined range agreed to for a certain investor or type of investor. Tightening concentration limits typically requires consent from the borrower.

Discussion

Fund borrowers often request a Concentration Limit Holiday when the fund is still in its fundraising stage and has not yet reached its target commitment size. During the early part of fundraising, the investor base will likely be more concentrated than after the final investor closing, since funds will often start with a few cornerstone or anchor investors and then expand from there until they reach their target. Application of typical concentration limits in a borrowing base at the early stage of fundraising could severely limit borrowing capacity and undermine the purpose of the line of credit.

When parties agree to utilize a Concentration Limit Holiday, the holiday will typically run from the initial closing to the earlier of the final closing of investors or a specific date after the initial closing (i.e., six months). The holiday may also be structured so that the applicable concentration limits change during the holiday period at agreed upon threshold dates. This provides another layer of flexibility so that concentration limits may be introduced progressively over the course of the holiday before reaching the final agreed concentration limits at the termination of the Concentration Limit Holiday. Setting a specific end date for the holiday provides certainty for the lenders, avoiding the risk that multiple extensions to the fundraising period will extend the holiday indefinitely. Lenders will naturally be more receptive to utilizing Concentration Limit Holidays where fund borrowers raise the point early during discussions and have had a strong initial round of fundraising.

These insights are based on data from subscription line facilities documented by Haynes Boone during the referenced period.

For more information on fund finance market trends, please reach out to any member of the Haynes Boone Fund Finance Practice Group.

For additional news and insights, please subscribe to our email list.